How to Sell Your Business and Plan an Exit Strategy in 2021

Selling your business can seem like a daunting process, especially if you’re unsure of whether it’s a good idea to sell in the first place.

To get the best price and ensure the smoothest transition for your business, you’ll need a careful plan for preparing to sell, completing the sale, and navigating your transition out of the company.

In this guide, we’ll take you through the most important considerations regarding when to sell your business, the key steps to selling your business, and tips for planning your exit strategy.

How to know when to sell your business

Some business sales are motivated by life circumstances: perhaps you’re looking to retire or simply reduce your responsibilities and focus on your family, health, or hobbies.

Other times, business owners looking to maximize their profits, mitigate their financial risks, or hand over the companies to more forward-thinking leadership.

When you’re deciding whether or not to sell your business, take some time to think through what’s motivating you. Your reason for selling will help influence the timeline of your business selling strategy.

For example, if you’re planning to retire at a certain age, you’ll want to begin the selling process at least a year in advance to make sure you can stop working on schedule.

But, if you’re looking to sell your business to maximize profits, it might make more sense to prepare your business for the sale and then hold until the market will yield an impressive payout.

7 steps to selling your business in 2021

Selling a business is sometimes a long and complex process. You’ll likely need to consult with lawyers, brokers, and potential buyers over a long period.

At the same time, you’ll need to make sure your business is in good shape and ready to be handed over to a new owner.

These seven steps will take you through how to sell your business, with practical tips for how to do it right.

Organize your paperwork

Before you can begin looking for a business broker or potential buyer, you’ll need to do some housekeeping behind the scenes.

Make sure all of your legal and financial paperwork is in order. You’ll need some of this information for the business valuation (more on that next). It’s also the first step in preparing your business for new ownership.

Here are a few documents you should gather:

- Financial paperwork like profit and loss statements or balance sheets

- Several years of tax returns

- Employment records or contracts

- Vendor or lease agreements

Essentially, think of all the various components of your business, like your property, employees, and profits, and gather any documentation that demonstrates their status.

If you maintain your paperwork on an ongoing basis, you’ll always be one step ahead of your exit strategy when the time comes to sell.

Get a business valuation

With your business paperwork pristinely organized, look for a business valuation expert who can estimate what price you’ll be able to get.

The valuation expert will take a look at your business’s assets and performance to determine its value. You’ll present the report to prospective buyers for additional credibility.

Remember that their estimated value is not the actual price of the business. The sale price still depends on market forces and other factors. Some buyers may be willing to pay more or less than the estimated value.

Boost sales and plan your exit

Once you have a business valuation completed, you’re ready to prepare your business for review by a broker and buyers.

The valuation report may show some weaknesses that you can address before looking for buyers. For instance, you might make staffing changes, pivot marketing strategies, or boost sales to make the business more attractive.

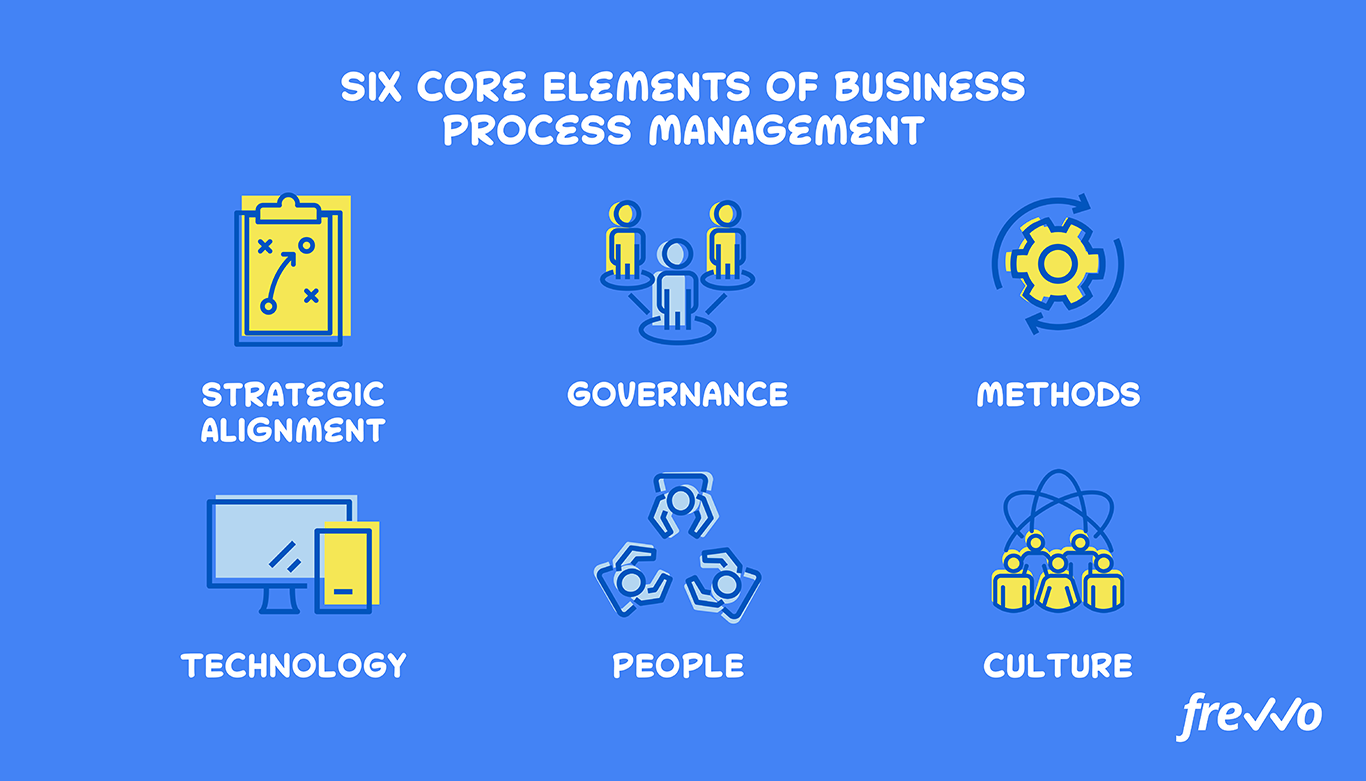

Now is also a good time to implement or revise your business process management (BPM) practices.

This approach turns your business practices into optimized processes that maximize efficiency. As you can see in the graphic above, BPM can cover everything from business strategy to your workplace culture.

If you want your business to continue running smoothly when you’re no longer at the wheel, formalizing or even automating some of your business processes can leave a strong legacy.

Find a reputable business broker

Unless you’re selling your business to a family member or someone extremely close to you, it’s smart to hire a business broker to help you find buyers and get the best price.

Think of brokers like real estate agents for your business. They’ll help you find the best possible price, screen potential buyers, and help you complete all the legal and financial components of the sale.

Business brokers often work on commission. When you’re looking for a broker, make sure you understand and agree to their commission structure, so you get the amount of money you need from the sale.

Meet with qualified buyers

Finally, it’s time to meet with potential buyers to find the right fit for your business. You’ll need to present and pitch your business to make a convincing sale.

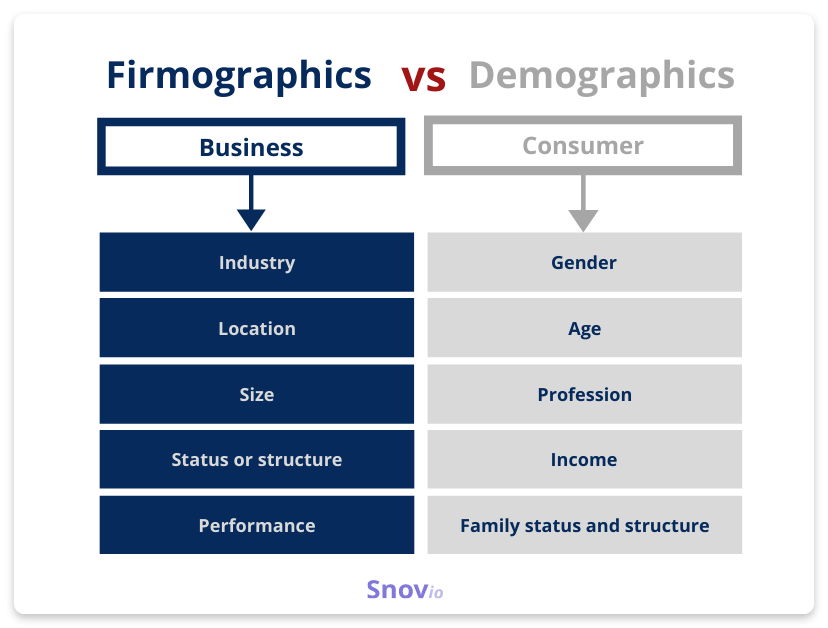

Before you meet with buyers, work with your broker to find the most promising and legitimate offers. Then, provide the interested parties with important company information like recent profits, current assets, and firmographic data.

Firmographic data is like demographic information for businesses, according to Breadcrumbs.io. It includes data points like company revenue, total employment, location, and even ad spend.

When presenting your company to buyers, provide the firmographic data of your own company so they can get a quick snapshot of your business. If you’re a B2B company, offer firmographic data on your customer base as well.

Finalize contracts

Completing a business sale means even more paperwork.

Once you’ve accepted an offer of sale for your business, you’ll need to sign and file several key documents to finalize the sale.

Some of these documents include:

- Purchase agreement

- Bill of sale

- Noncompete agreements

- Asset listings

Whether or not you hire a business broker, you should hire a lawyer to help with the legal side of the paperwork to avoid any problems down the line.

If you’re selling your business to stakeholders that aren’t local to your area, keep the paperwork process simple and easy by using document signing software. Rather than dealing with tedious scanners or even fax machines, everyone can access, review, and sign the same document.

Tie up loose ends

Now it’s time to wrap up your involvement in the company and follow through on your exit plan.

As you hand over ownership, you may need to hold transition meetings, make internal or public announcements, and transfer any knowledge or assets you may have over to the company.

Once you’ve checked the last item off your to-do list, take some time to celebrate — you just sold your business.

5 tips for planning your exit strategy

Your exit strategy encompasses all of the tasks and decisions related to selling your company and stepping down from leading it.

Every exit strategy will look different, depending on your role in the day-to-day operations. No matter how involved you are, you can use these tips to plan the right exit strategy for eventually selling your business.

- Start planning your exit way in advance. Even if your business is brand-new, think about what you’d do if that perfect offer came across the table.

- Think about your family and long-time employees. If you distribute any company assets as gifts to your family or staff, make sure they’re structured as tax-deductible gifts.

- Be flexible. You never know what circumstances will pop up around your business sale, so be open to new possibilities and opportunities.

- Update your strategy regularly. Social and economic forces, as well as your personal preferences, might change your ideal exit strategy. Review your strategy regularly to make sure you’re always prepared.

- Mentor your employees. If you fill a significant role in company operations, make a habit of mentoring your employees so you can pass on your skills and knowledge. If they stay with the company after the sale, your expertise will live on in your team.

Sell your business smoothly

Selling your business is a complex process, but it doesn’t have to be a headache. With early, careful planning, you can design a smooth sale and exit strategy. You’ll be able to sell it at the right time to get the best possible price.

Author Bio

Reid Burns has his roots in the supply chain, handling global teams for private label companies. He has since transitioned to freelance work, providing thought leadership in the e-Commerce domain.

{kind=link}